Become an Enrolled Agent: Step-by-Step Guide

Passing the Enrolled Agent (EA) exam opens the door to...

If you’re planning to take the SEE, you need to have comprehensive Enrolled Agent study material to help you prepare for the IRS Enrolled Agent exam. But how do you know if you’re ready to take the SEE?

Enrolled Agents are federally authorized tax practitioners who can represent taxpayers before the IRS. To become an Enrolled Agent, one must pass the Special Enrollment Examination (SEE). The exam covers a wide range of tax-related topics, from individual and business tax returns to representation, practice, and procedures.

Here are some example questions that will give you an idea of the type of Enrolled Agent study material that is covered on the exam:

Which of the following is an example of a common tax credit that is available to individuals?

a. Alternative Minimum Tax Credit

b. Child Tax Credit

c. Domestic Production Activities Deduction

d. Health Coverage Tax Credit

When can a taxpayer make a contribution to a traditional IRA for a particular tax year?

a. Anytime during the tax year

b. By the end of the tax year

c. By the due date of the tax return, without extensions

d. By the due date of the tax return, with extensions

What is the maximum penalty for failing to file a partnership tax return by its due date (including extensions)?

a. $195 per month for each partner

b. $195 per month for each partner, up to a maximum of 12 months

c. $195 per month for each partner, up to a maximum of 5 months

d. $205 per month for each partner, up to a maximum of 12 months

Which of the following entities is not required to pay estimated taxes?

a. A sole proprietorship

b. A partnership

c. A corporation

d. An S corporation

Which of the following is a requirement for a taxpayer to claim a dependent on their tax return?

a. The dependent must be a U.S. citizen

b. The dependent must be a relative of the taxpayer

c. The dependent must live with the taxpayer for at least half the year

d. The dependent must be a full-time student

If you find these questions challenging, don’t worry. They are just a small sample of the type of material covered on the SEE. However, they give you an idea of the level of knowledge and preparation required to pass the exam.

To ensure your success in passing the SEE, it’s important to have access to quality study material. Enrolled Agent study material such as test bank questions, practice exams, mini-exams, Power Notes, dynamic textbooks, and more can help you get familiar with the material and the exam format.

In conclusion, becoming an Enrolled Agent can be a rewarding career choice for those with a passion for tax law and a desire to help taxpayers navigate the complex tax system. By taking sample IRS SEE questions like the ones provided above, you can determine your readiness for the exam and take steps to prepare accordingly with the right study material.

Here are five more test question examples for the IRS Special Enrollment Examination (SEE):

Which of the following types of tax return preparers must obtain a Preparer Tax Identification Number (PTIN) in order to prepare tax returns for compensation?

a. Enrolled agents

b. Attorneys

c. Certified public accountants (CPAs)

d. All of the above

What is the maximum amount of time that an offer in compromise (OIC) can be placed on hold by the IRS before it is rejected?

a. 6 months

b. 12 months

c. 18 months

d. 24 months

Which of the following types of taxpayers are required to use the accrual method of accounting?

a. Corporations with gross receipts over $25 million

b. Partnerships with gross receipts over $25 million

c. Sole proprietors with gross receipts over $25 million

d. All of the above

Which of the following penalties is not applicable to an enrolled agent who fails to comply with Circular 230 requirements?

a. Monetary penalty

b. Suspension from practice before the IRS

c. Revocation of enrolled agent status

d. Imprisonment

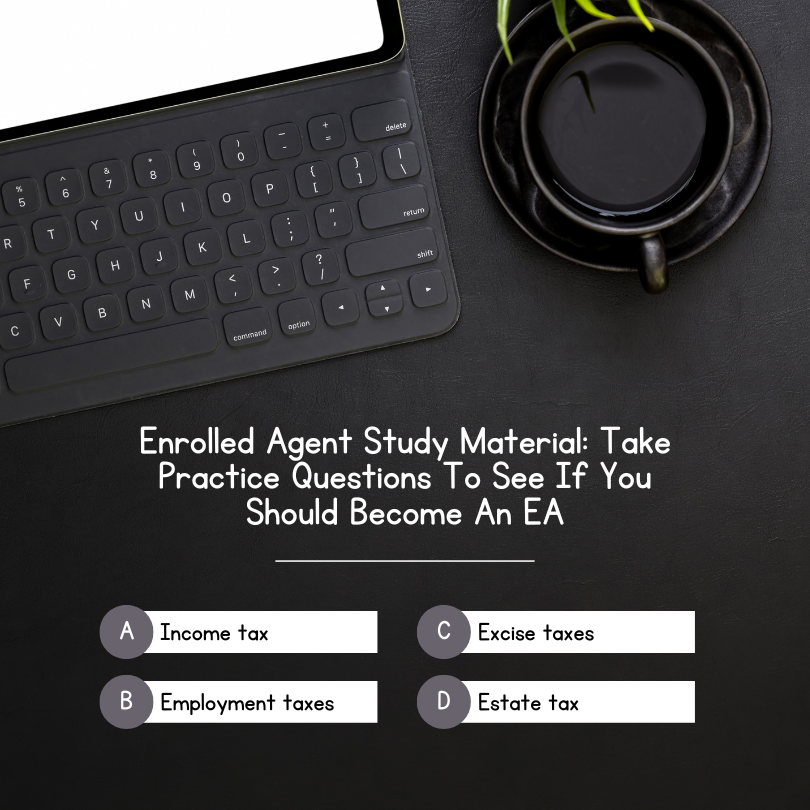

Which of the following taxes is not subject to the Federal Tax Lien?

a. Income tax

b. Employment taxes

c. Excise taxes

d. Estate tax

Note: The actual SEE may contain questions that are more complex and require more extensive knowledge than the examples provided here.

First set of questions:

Bonus questions:

Passing the Enrolled Agent (EA) exam opens the door to...

The journey to becoming an Enrolled Agent is both challenging...

Imagine gazing at a promising future as a tax professional.However,...

Achieving the status of an Enrolled Agent is a significant...

Are you envisioning a successful career as an Enrolled Agent?It's...